Trusted by over 400,000 with their insurance needs

Our service is rated ‘Excellent’ on Feefo

")

Over 2000 insurance specialists ready to support you

How to find the value of your classic car

How to find the value of your classic car

We explore how to find the value of your classic car with the help of Patina. If you're buying, selling or looking for classic car insurance this helpful resource has plenty of data to help you establish the value of your classic and whether it's increasing or decreasing in value.

What is my classic car worth?

Some classic cars will appreciate in value breaking away from the traditional market value trend. To discover the true value of a classic car you should take into consideration:

-

History

-

Prestige

-

Condition

-

Original features

-

Concourse

-

Awards

-

Popularity

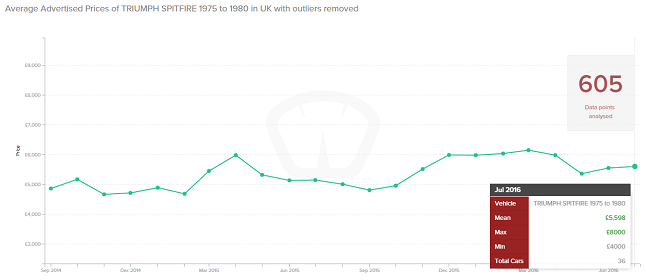

We’re going to use one of our favourite classic cars as a real life example to guide you through the process step-by-step. We've chosen a triumph classic car, the Triumph Spitfire 1500 pictured above.

It's best just to use the make model and year of your classic car to find the trends of similar models. As the Triumph Spitfire was manufactured from 1975 - 1980 we used those dates.

Why is insurance for classic cars different?

Regular car insurers either provide cover on a new for old or market value basis. Classic cars on the other hand, have both tangible and intangible assets which add value to the vehicle. For example, you’d expect a car with fully functioning original features to be worth more than one where some of the features have been broken or replaced. Equally, a car once driven by someone famous or with an interesting history should demand a higher price. Classic cars are therefore more accurately insured on an ‘Agreed Value’ basis.

What does agreed value mean?

Agreed value is a term used for when the insurer and insured agree on a unique value for an item rather going by the cost of an equivalent as new (new for old) or the current cost (market value). Agreeing a value means looking at other factors which can affect the vehicles price tag; these can be both tangible and intangible. When insuring a classic car this takes into account aspects such as concourse, awards, history of the vehicle and prestige (e.g. first off the production line, special edition etc.).

Why is agreed value important?

If your classic car were written off in an accident, you'd want to ensure you could get a replacement. By taking into account the true cost of replacing your classic car, you're ensuring that if the worst happens, you have enough cover in place to get yourself back on the road in something just as classy.

If you need to find Triumph classic car insurance you can get a quote online through our partners at Footman James.

About the author

Chris North FCII is a respected industry leader with over 40 years' experience, who has worked in the insurance industry in a variety of roles, accumulating a wealth of knowledge. He is currently Technical Manager for Towergate's motor division, providing expertise on all matters relating to motor fleet insurance, in particular haulage and self-drive hire fleets.

Chris North FCII is a respected industry leader with over 40 years' experience, who has worked in the insurance industry in a variety of roles, accumulating a wealth of knowledge. He is currently Technical Manager for Towergate's motor division, providing expertise on all matters relating to motor fleet insurance, in particular haulage and self-drive hire fleets.

Date: July 18, 2017

Category: Motor

")

")